The raise hit my account and, weirdly, nothing changed. I was earning more, but by the end of the month I still checked my balance before ordering food. Rent was higher. The car EMI was higher. Even my “small treats” somehow added up to a number that scared me when I finally looked.

That’s the part nobody warns you about. You don’t suddenly become reckless. You just slowly adjust your life upward until your money can’t breathe.

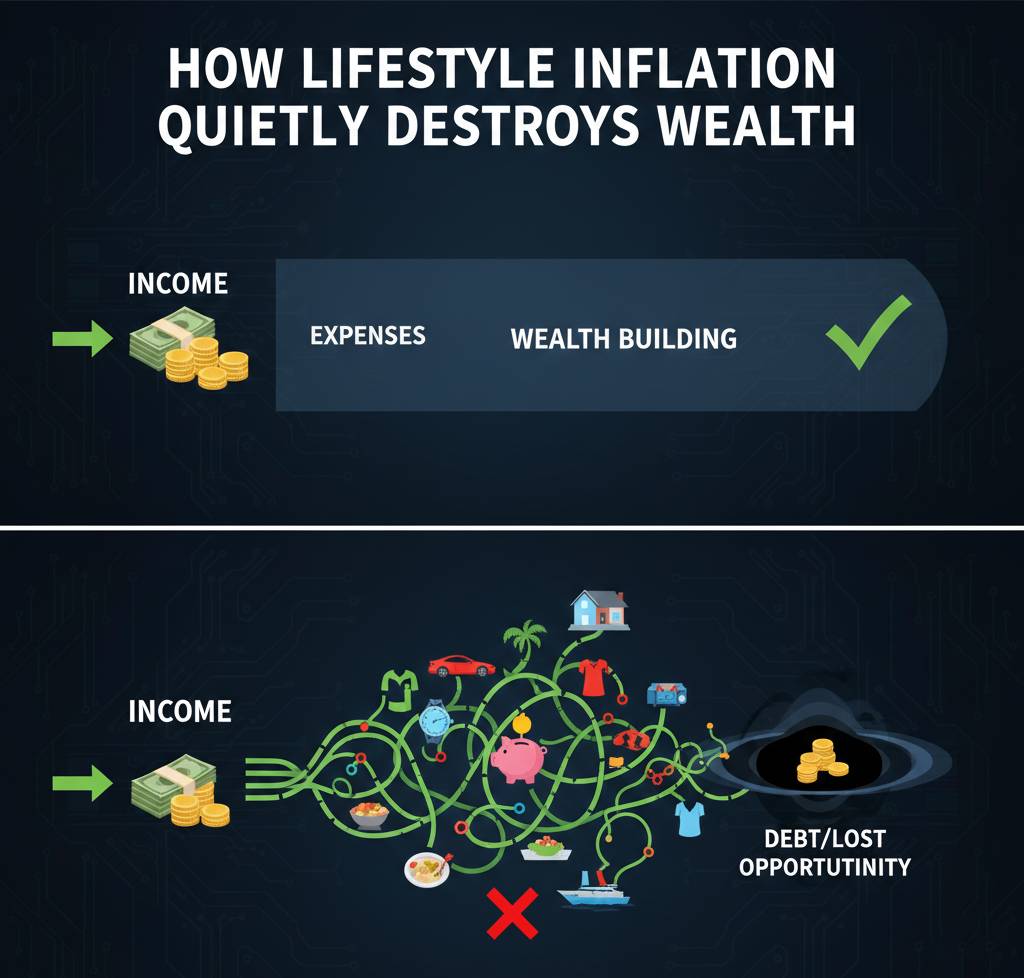

“I can afford it now” is where it starts

The first upgrade usually feels logical.

- You move to a better place because the old one feels cramped.

- You switch phones because work “needs” it.

- You start eating out more because time feels scarce.

Each choice makes sense on its own. I remember telling myself, this is what progress looks like. The problem is, progress quietly turns into a permanent cost.

Once a higher expense becomes normal, it’s very hard to go back without feeling like you’re losing something.

Why lifestyle inflation is so hard to notice

From what I’ve seen, lifestyle inflation doesn’t announce itself. There’s no moment where you say, “I am now overspending.”

It hides in:

- subscriptions you don’t cancel

- EMIs that felt manageable at the time

- convenience spending you justify as “mental peace”

Because income is rising, there’s no immediate pain. That’s why it’s dangerous. The damage shows up years later, not months later.

A real example that still annoys me

A friend of mine doubled his income over four years. On paper, he should’ve been in a great spot.

What actually happened:

- bigger apartment

- second car

- international trips on credit cards

- gadgets upgraded every year

When he wanted to take a break from work due to burnout, he couldn’t. His fixed expenses were so high that even three months without income felt impossible.

That’s the real cost people don’t talk about. Not being “poor,” but being trapped.

The biggest mistake I see again and again

People tie lifestyle upgrades directly to income upgrades.

No pause. No question. No buffer period.

This is where advice online often breaks down. You’ll hear things like “enjoy your money” or “you earned it.” Both are true. But nobody talks about timing.

Upgrading everything at once locks your future self into decisions your present self made without full context.

Wealth isn’t about how much you earn day-to-day

This took me a long time to really get.

Wealth is about:

- how long you can survive without income

- how flexible your choices are

- how calm you feel when money surprises show up

Lifestyle inflation attacks all three.

High income with high fixed costs feels impressive from the outside but fragile from the inside. One job loss, one health issue, one bad year—and everything shakes.

The emotional side nobody mentions

There’s also a quiet anxiety that comes with it.

When your lifestyle depends on your current income:

- every performance review feels heavier

- every market slowdown feels personal

- every unexpected expense feels like a threat

I’ve seen people earning well but sleeping poorly because their lives were built on a narrow margin.

Personally, I don’t think that trade-off is worth it.

“But what’s the point of earning more then?”

This is the pushback I hear most, and it’s fair.

The point isn’t to live like a monk. It’s to upgrade selectively.

The people who seem calm with money usually:

- upgrade slower than their income grows

- keep big expenses boring

- spend freely only in areas they truly care about

They don’t look flashy. But they also don’t panic.

How long it actually takes to undo lifestyle inflation

If you’ve already inflated your lifestyle, reversing it isn’t quick.

From what I’ve seen:

- canceling subscriptions is instant, but emotional resistance is real

- changing housing or cars can take months or years

- adjusting spending habits takes sustained awareness, not willpower

This isn’t a weekend fix. It’s more like a slow reset.

Where advice often becomes unrealistic

A lot of content treats lifestyle inflation like a moral failure. It’s not.

It’s human behavior mixed with social pressure and delayed consequences.

What doesn’t work:

- extreme frugality overnight

- shaming yourself for past choices

- pretending income will always rise

What works better is noticing where money stops adding happiness and starts adding stress.

Things worth checking (without turning it into rules)

If you’re thinking about this honestly, a few reflections usually help:

- Which expenses would be hardest to cut if income stopped for six months?

- How many upgrades were decisions vs defaults?

- Are your biggest costs aligned with what you actually value, or just what looks “normal” now?

Practical considerations people underestimate

Some things matter more than people think:

- fixed costs matter far more than occasional splurges

- flexibility beats optimization

- boring financial choices often create the most freedom later

And some things matter less than people think:

- impressing people who don’t see your bank balance

- matching peers who are also guessing their way through money

- constant upgrading just because something new exists

What to be careful about

Be especially cautious when:

- income jumps suddenly

- expenses are justified as “temporary”

- decisions are rushed during high motivation phases

Those are the moments where lifestyle inflation locks in fastest.

Final thought, not a formula

There’s no single right way to live. Some people value comfort now. Some value options later. Most want both.

Just know this: lifestyle inflation doesn’t ruin wealth loudly. It does it quietly, over time, while everything looks fine.

And by the time it feels heavy, undoing it takes patience, not hacks.