Inflation: Why the Numbers Lie and Your Gut Is Right

You know that feeling when you check your savings account balance and it looks like it’s grown a little, but somehow everything at the grocery store feels way more expensive? That’s not just in your head. That gut feeling you’re having—that your money isn’t stretching as far—is the exact thing we need to talk about.

It’s called inflation, and if you don’t get how it works, you’re basically planning your financial future with faulty math.

Here’s the blunt truth I learned the hard way: seeing a number go up in your bank account is meaningless if you don’t know what that number can actually buy.

A few years back, I was patting myself on the back for hitting a savings milestone. Felt great. Then I tried to use that “milestone” for a down payment I’d been eyeing for years, only to find the goalpost had moved. The price had jumped. My neat little pile of cash was now worth less in real terms.

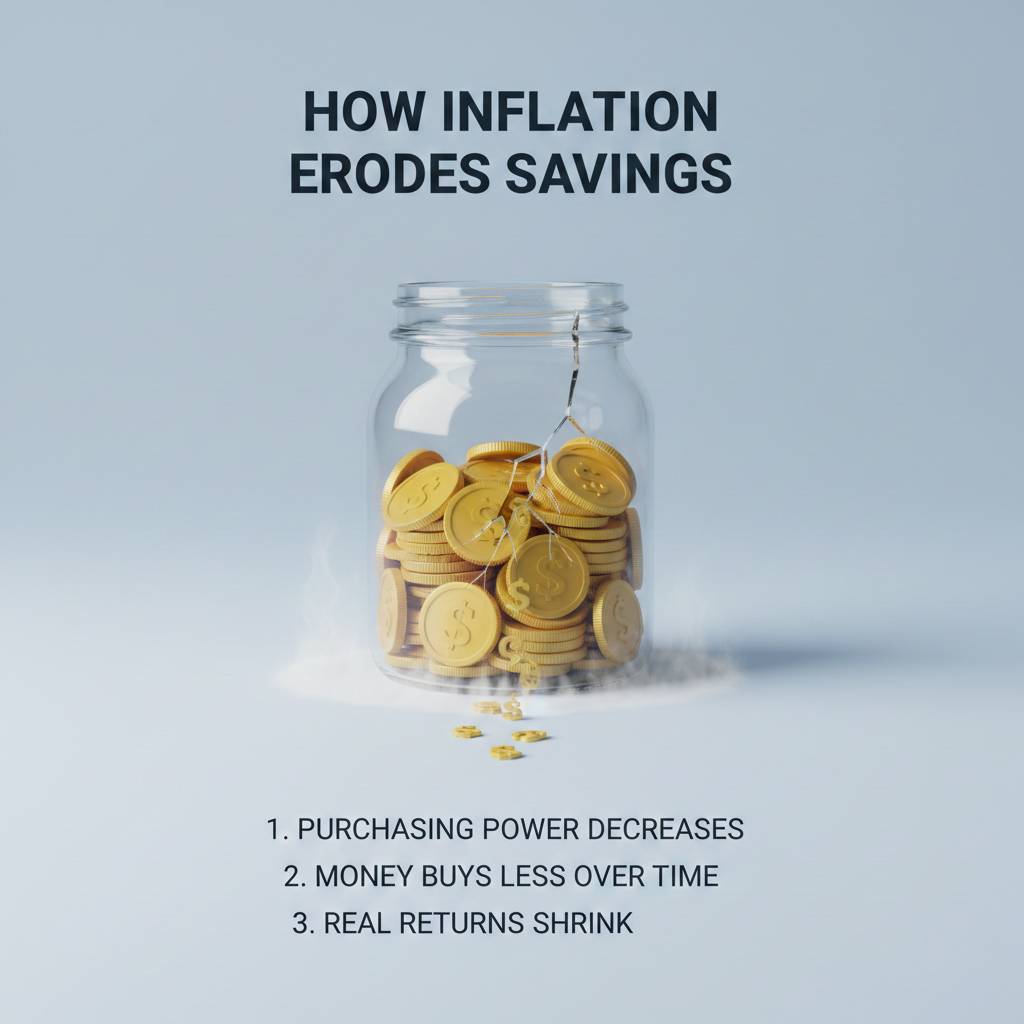

I hadn’t lost a single dollar, but I’d lost a chunk of its power. That’s the silent tax nobody sends you a bill for.

It’s Not About Dollars, It’s About Buying Power

Forget the textbook definition. Think of inflation like this: it’s the rate at which your money becomes less potent. If inflation is 3% this year, that basket of groceries that cost you $100 last year now costs $103.

If the cash in your savings account only earned 1% interest, you’re falling behind. You have more dollars, but less stuff-buying ability.

This is where almost everyone, including my past self, gets tripped up. We focus on the nominal value (the number on the screen) and ignore the real value (what it can actually do for us).

Making this mental shift is the single most important step. You start asking: “Will this money in the future buy the same, more, or less than it can today?”

Why Online Inflation Calculators Are Your New Best Friend

You don’t need a finance degree for this. You need a simple tool and five minutes. I’m talking about online inflation calculators—like the CPI Inflation Calculator from the U.S. Bureau of Labor Statistics or similar tools on financial education sites.

These tools do one crucial thing: they translate past or future dollars into today’s money. It’s the closest thing to a time machine for your finances.

How I Actually Use Them

- The reality check: I once considered leaving a chunk of cash in a super “safe” savings account earning almost nothing. I used a calculator to see what $10,000 from 10 years ago would be worth today. The answer—roughly $7,800 in buying power—killed the illusion of safety instantly.

- Planning for real goals: Say you want $30,000 for a project in 10 years. With 3% average inflation, you don’t need $30,000—you need about $40,300 to have the same buying power. That changes the goal completely.

You’re no longer saving for a number. You’re saving for a level of purchasing power.

Common mistake: People run these calculators once, feel bad, and never touch them again. The real value comes from using them before you set a goal or celebrate account growth.

Where These Tools Fall Short

Inflation calculators aren’t magic. They rely on averages, usually based on the Consumer Price Index (CPI). Your personal inflation rate may be very different.

If you drive a lot, fuel costs hit harder. If you rent, housing dominates your budget. The calculator won’t capture that perfectly.

I made the mistake of treating the output like gospel. It’s not. It’s a benchmark—a very useful one—but still a benchmark.

These tools also don’t factor in your investment returns. Their job is to show you the hill. Your job is to find a way to climb it.

What This Changes in Real Life

- Your “safe” cash gets questioned. The biggest risk isn’t always market crashes. It’s slow, invisible decay.

- Your goals get smarter. You stop aiming for random numbers and start targeting today’s buying power.

- You spot hollow advice instantly. A 5% return during 7% inflation is a loss. No debate.

Rising prices create anxiety. But not understanding inflation creates helplessness—and that’s worse.

Spending ten minutes with an inflation calculator won’t lower your bills, but it will show you the rules of the game you’re already playing. Once you see that clearly, your plans finally have a fighting chance.

Disclaimer: This article focuses on understanding how inflation affects purchasing power. Decisions about saving, investing, or protecting money involve personal risk and should be based on your own research or professional financial advice.